Embracing a new normal

Crypto's increasing importance in a post-COVID era

(Re)Introduction

So we are back after a bit of a longish hiatus.

But first, an update and some explanations for our prolonged absence.

To write a daily newsletter is a significant investment in time, with little in terms of immediate payoff, except, arguably some self-actualization. A few months ago, as our publishing frequency kept dropping, folks increasingly reached out to check if we were OK. Thankfully, we are as OK as can be, in these uncertain times. However, the sheer number of folks reaching out to us to check in on what happened to the Satoshi & Co new made us realize that we were indeed providing value to a lot of folks, especially those that did not actively follow crypto. One thing that we have in crypto is a surfeit of literature for folks that are already immersed in this space. The other thing is that writing a newsletter everyday, as everyone from @howardlindzon to @matt_levine will tell you, is the best way to make sure you yourselves are on top of whatever space you are in.

With the motivation clearly established, it is a matter of figuring out where to squeeze out the 90 to 120 odd minutes it requires on a daily basis, in between whatever we do for a living. Predictably it has to be either very early in the day, or deep in to the night, when we actually get the opportunity to do this undisturbed ‘deep work’, as Cal Newport calls it. With some regularity, this hopefully becomes an effort that is closer to 60 minutes than 90, and that is the rhythm that we aim to get to over the next few weeks and months. The idea is to inform an already rich debate with some specific viewpoints that we develop over time, and some unique experiences that we gather with our work in crypto, and with a vantage point straddling Asia and the US. At all times, we will strive to keep this interesting.

Also, some housekeeping…

- We have moved from Revue to Substack. Revue is great, but we wanted to give Substack a whirl, and it helps that Substack website is ‘slightly’ more user friendly and has a more active crypto community. Revue is not quite a destination in the way that Substack or Medium is. It is always a bit of a danger trying to port over 30,000 subscribers, but I mean, you gotta do what you gotta do, and if folks like the newsletter, they will pardon the mild inconvenience and continue to be with us! Please make sure you mark our emails as ‘not spam’ in your inbox filters, should you wish to receive this on a daily basis of course, which we hope you really do!

- We will periodically have thought pieces from experts/practitioners in the crypto space, another reason for you to check in on us regularly

So with that context out of the way, we start with our first Satoshi&Co substack edition. We will stick to our traditional format of the overall scan, along with one thematic deep dive on most editions, with deep dive sometimes being really deep, and sometimes just a broad brush stroke.

Today, we go all macro.

On Liquidity, ZIRP, global macro ( and BTC)

Key takeaways

Liquidity increasing; The US dollar may or may not continue to be relevant, money printing might stop or it might not, but in any scenario, BTC (and ETH) look increasingly attractive for two key reasons: One direct driver - the secularly increasing/expanding search for yield, and another indirect but possibly stronger driver- the increasing complexity of the global economic order which directly benefits crypto assets

In one of our earlier editions, sometime in late January before going into the Chinese lunar new year, we had made two predictions. One, that there would be a glut of liquidity in the global markets, which would lead to more inflow into the riskier asset classes, including bitcoin. Remember, this was a pre-COVID assessment. Two, we had underestimated the then-emerging threat of the Corona Virus, and had assumed that the Virus would go the way of the SARS virus early on in the millennium. That calls for a big slice of humble pie.

However, the liquidity prediction was spot on; as a response to the Covid crisis, central banks around the world have doubled down on already aggressive stimulus programs, and the global economy is awash in liquidity, mostly from ‘helicopter money’ as Milton Friedman described such policies. The overall stimulus package across the world is currently estimated to be over USD 25 Trillion. To put that number in to perspective, note that last year, the size of the overall global economy was around USD 87 Trillion. The stimulus packages employ pretty much every trick in the banker tool kit; balance sheet expansion through asset purchases, loan guarantees, rate cuts, direct cash hand-outs as well as spending pledges.

Unfortunately though, at the moment, the only place that these measures are having an impact are in the financial markets. Lockdowns are affecting businesses and economies around the world in an unprecedented manner still, and perhaps the stimulus is preventing a bad situation from getting worse, if one were looking were straws to clutch on to. Regardless, we have an interesting situation where the markets, across asset classes, are completely out-of-synch with the real state of the economy. Even as GDP outlooks are slumping to levels not seen in decades across economies around the world, the markets in most of these places are going from strength to strength. Is this suspension of disbelief a la Wil.E.Coyote or is this the market pricing in a fairly quick turnaround over the next couple of quarters?

The pessimists, including Ray Dalio of Bridgewater, believe this is a lost decade for equities especially, as consumer demand struggles to recover to pre-Covid levels after a ‘hysteresis’ shock changes behavioral patterns significantly, in the way people live and work and eat.

The counter argument of course is that it took the US stock market just five years, in 2012, to surpass its previous highs from 2007, pre-credit crisis levels. Even in the moderately optimistic scenario, with advances in the vaccine development process, and with some form of moderate herd immunity, suppressed demand could come bouncing back, and with some form of active involvement from the 1% as well, the world might find itself back on its feet sooner rather than later, perhaps even by mid-2021. However, you wouldn’t want to bet the farm on this scenario.

There is another rabbit hole that any liquidity/stimulus related discussion invariably descends into. How long can the US continue to print money? Perhaps it does not really matter, since it is all relative. After all, Money is an abstract social construct signifying relative purchasing power among entities. If the major global currency blocs - say US, China, Europe, and Japan for now, get together and decide to accelerate spending and expand balance sheets as a response to the current crises, arguably the relative positions of their currencies does not change that much. The side effect will of course be extreme volatility in Emerging Market currencies as these try to adjust to the new market-driven peg. Also with the Zero-Interest-Rate-Policies (ZIRP) practiced by the big blocks, any public debt can also continue to be rolled over indefinitely. Therefore, there are better uses of time than speculating into when and how this continuous money-printing, especially by the US, will end. It might happen at some point, most likely as a result of something China-related. The markets can however remain irrational for a long time, and in the long run, we are all dead.

Irrespective of where you think the economy is going to end up in a year or two from now, it makes sense to remember that in either scenario, crypto will likely do well; Thanks to the endless search for yield that the ZIRP regime perpetuates.

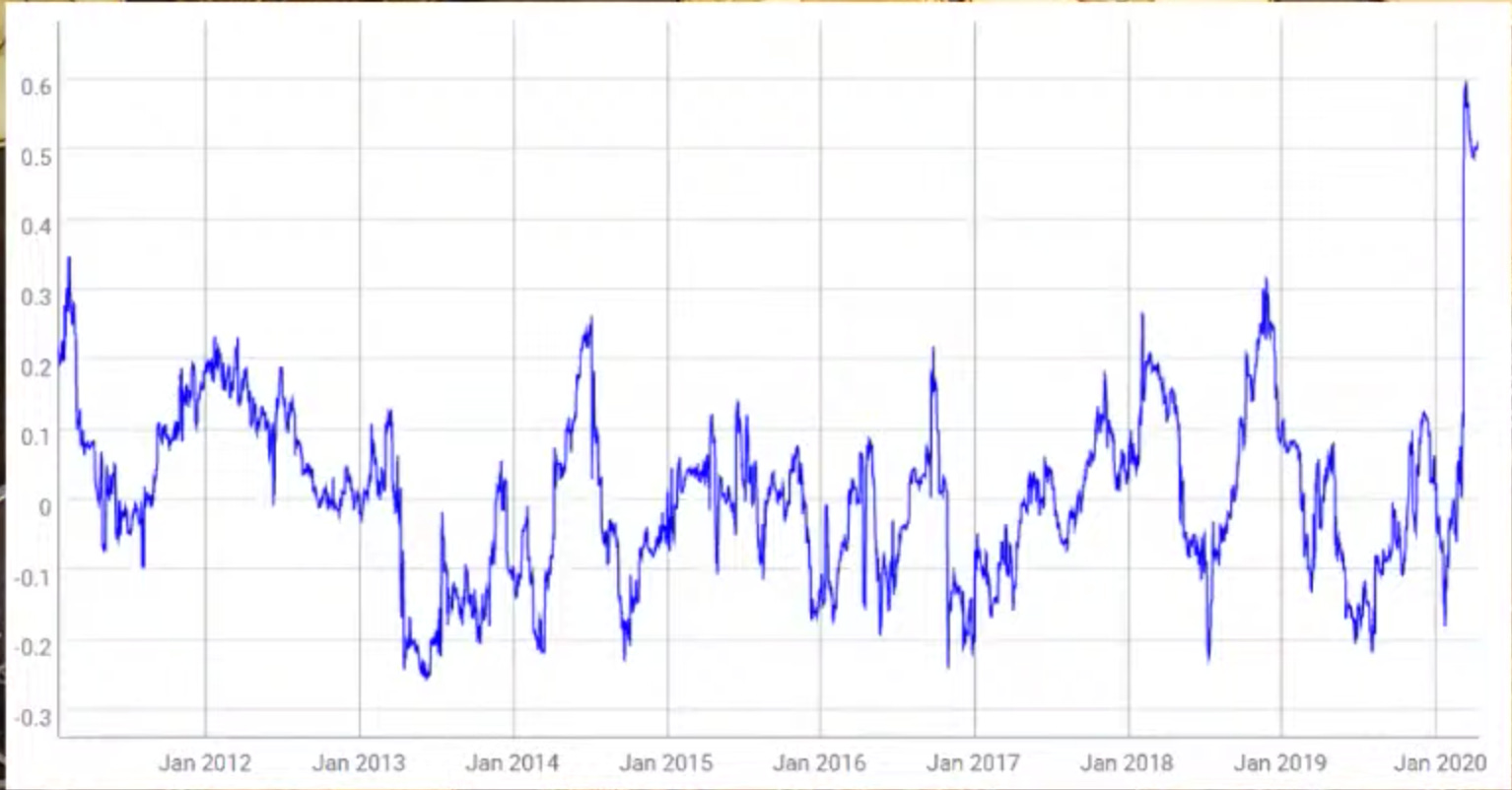

Pension and endowment plans around the world, which are the key driver of capital inflows into markets, including alternative assets such as venture capital and private equity continue to be massively underfunded. Their expected cashflows are already not enough to meet their obligations. The ZIRP regime will make their task even more difficult, unless they aggressively look at diversifying into assets that can generate a higher yield. As we explored in an edition earlier this year, adding a little bit of BTC to a portfolio does wonders to its Sharpe ratio. BTC is also far more liquid than something like say, a VC investment or a private debt position. As the hunt for yield intensifies, it is inevitable that more and more of such institutional capital starts spilling over to asset classes that were easier deemed to be too risky or marginal. This was the case with VC and PE in the early 90s, and this is what is now happening with BTC. There is some indication that this process is already underway - witness the increasing correlation between BTC and the S&P over 2020. This is clearly a sign of institutions bucketing BTC as a legitimate asset class along with equities and moving in and out of it, depending on whether it is risk-on or risk-off.

Correlation between BTC and S&P 500 (Source - Coinmetrics)

Over the course of 2020, BTC price has been building up steadily and has settled into a range between 8.8k and 10k, up from its low of around 5k in Q1. Although the much-expected halving pump did not happen to its full extent, potentially due to the emergence of derivatives trading, all past indicators seem to point to a further increasing price trend post-halving over the next few years leading up to the next halving, expected to be in 2024.

Derivative volumes (and option volumes) have been on a tear, indicative of increasing institutional interest. Derivative volumes hit a high of $602 Billion in May, as per data from Cryptocompare. Stablecoin volumes have been increasing, aided by speculation that various countries, including China have been exploring ways to develop national digital currencies (See graphic below). DeFi (Decentralized Finance), with its emerging potential to reinvent modern banking, lending and trading, is slowly but surely emerging into the mainstream, just like BTC die four or five years ago. The amount of ETH locked up in DeFi, a key measure of the growth of DeFi, has been surging. While it is not a linear, one-to-one effect between DeFi and ETH price, it is safe to assume that as DeFi becomes increasingly important and traditional financial institutions as well get into the game, ETH being the infrastructure layer will also end up becoming the gateway crypto for all DeFi users. Interestingly, the emergence of ETH also provides an opportunity for BTC that is currently being HODL-ed in wallets, to be deployed to earn yield after conversion to WBTC (Wrapped BTC). The deflationary nature of bitcoins means that there will be a surge of interest in bitcoin in high-liquidity regimes like the one we are in currently. Indiscriminate money printing by various central banks have reduced real interest rates to near zero in many places. Disruptive conditions that made bitcoin hugely popular in places such as Venezuela, Argentina, Zimbabwe, Iran etc are now emerging in more marginal geographies across the world. ‘Six-sigma’ events now occur once every decade; we have had three big financial market events that have impacted the world just in the past twenty years, and we are sure to have at least as many in the next two. The next major crisis, likely a climate-driven one, will probably be upon us sooner rather than later. The Covid-related disruption is also throwing into sharp relief the emergence of China as a global power, albeit still one that is yet to come to terms with the responsibility that this entails, and the fault lines that this is causing has far-ranging repercussions. It is worthwhile to remember that a combination of the Great Depression and Hyper inflation brought about the last World War. Bitcoin, thanks to its anti-fragile nature, gains from the uncertainty that characterizes current times.

Stablecoin volumes have been increasing steadily. Again, it would be idle speculation putting any timelines on potential de-dollarization of the global economic order. Contrary to expectations that ETH and BTC will threaten USD dominance, ETH and BTC could potentially help strengthen the dollar’s status as the world’s reserve currency; It is a paradox of the current times that you have the central banks printing out money non-stop, but the demand for dollar around the world continues unabated. With the stable coins, whether they be collateralized through ETH like DAI, or through fiat currency with Tether, there is a far more reliable mechanism for the recording and settlement of global dollar flows when compared to the traditional fiat systems and its dependence on the Federal Reserve.

Heads crypto wins - Tails crypto wins

Crypto is an anti-fragile asset, poised to gain irrespective of how the future pans out

We live in extraordinary times. What is however abundantly clear is that the irrespective of the state of the world we end up in, it will be a new normal, characterized by increasingly polar debates amplified by the social media echo chamber symptomatic of the current times. In addition to the glut of liquidity, the inherently increasing entropy of the system seems to naturally favor accelerating inflows into ‘transnational’ assets such as gold and crypto that have value across borders. Volatility increases the value of crypto as an option. We thus have an increasingly complex economic order where crypto becomes an ‘essential’ asymmetric bet, and a critical component of every portfolio, large or small.

Linking around some interesting things we found on the web

UK fintech major Revolut is crossing the pond and offering crypto to users in the US; Even as DeFi volumes surge, there are concerns around improper practices around the emerging area of Initial Dex Offerings (IDO), as seen with the recent BZRX launch; China is testing the digital yuan through Meituan-Dianping and couple of otherTencent-backed company. Stablecoin volumes are increasing, the town of Tenino in Washington state is printing its own money, in a move that is not unprecedented. Cryptoderivatives exchange Bitmex is rebranding its holdco into a new entity called the 100x group

(Customary caveats - not financial advice, do your research; you can reach the author on twitter @cryptoman_ram and on LinkedIn )

This newsletter goes out to over 30,000 subscribers around the world most days of the week. Subscribe now to get this delivered to your inbox regularly

https://thehustle.co/covid19-local-currency-tenino-washington